Fintech is a combination of the two terms “finance” and “technology”. It refers to a business that uses technology to amplify financial services and processes. Fintech is a fast-growing industry serving both consumers and businesses. It has very broad applications like mobile banking, insurance, cryptocurrency etc and has made financial sectors safer, faster and more efficient by integrating technologies like AI, data science and blockchain.

There are some key changes taking place in Fintech-

- Dematerialization: Banking and insurance services distributed through the internet, telephone and agents.

- Disintermediation: Peer-to-peer models where savers directly lend to borrowers.

- Disruptors: Nonbanking institutions and insurance companies offering electronic money (eg- Safaricom in Africa), credit and savings services. Examples of disruptors- Facebook, MTN.

- Convergence: Banks and insurance companies converging, banks and disruptors partnering or merging (Orange’s acquisition of Groupama.)

- Blockchain: A series data, managed by a cluster of computers not owned by any single entity. The blocks of data are secured and held to each other using cryptographic principles (i.e. chain).

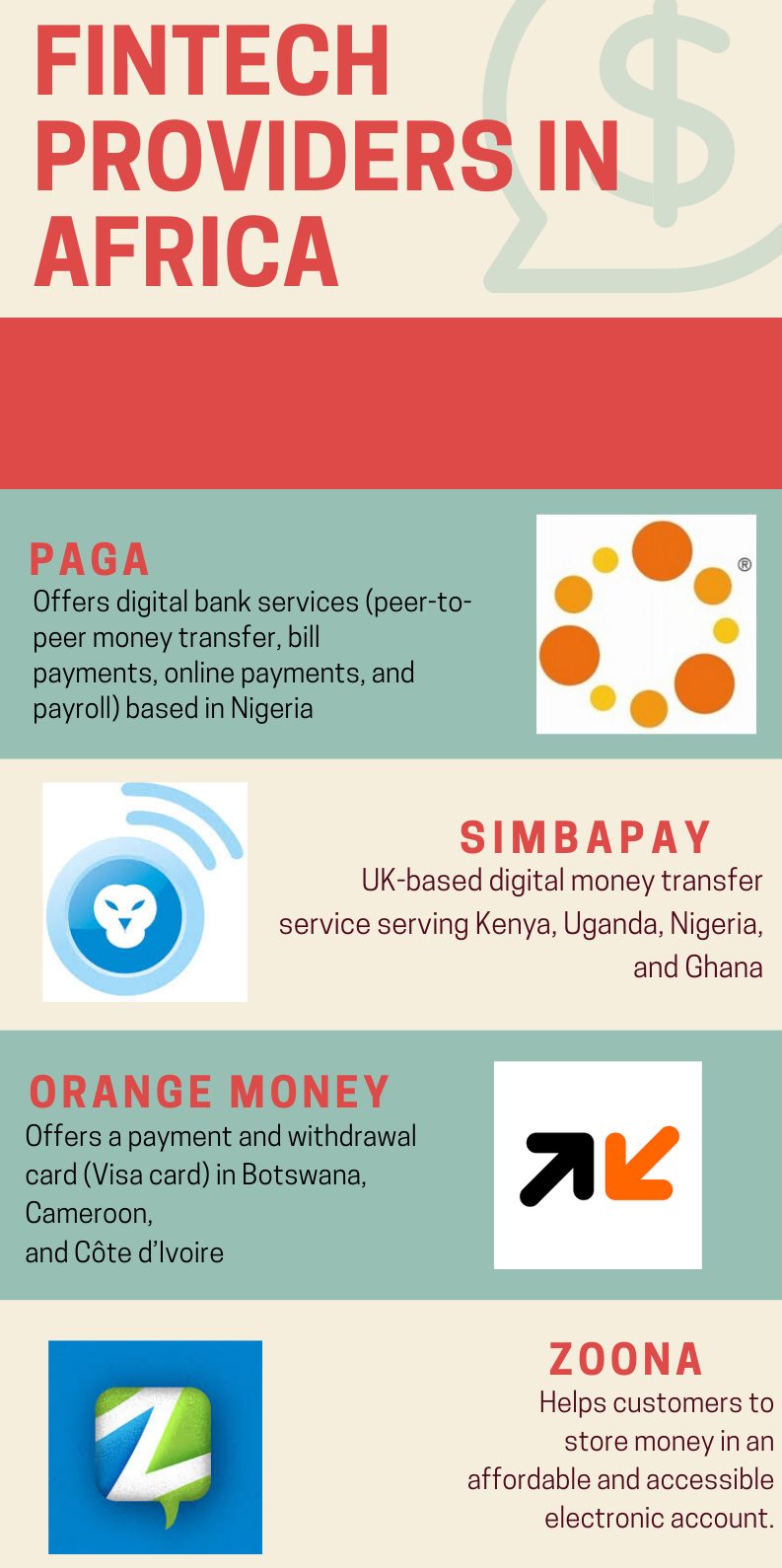

Fintech in Africa

In recent years Fintech has played a huge role in shaping the financial structure of sub-Saharan Africa’s financial sector. With rapid advancement in technology Fintech has challenged the traditional structures by creating efficiency gains. In sub-Saharan Africa, Fintech is enabling financial integration and serving as a catalyst for infrastructural and agricultural development.

Some of the most unbanked regions in the world can be found in Africa. But the wave of digital banking applications is bringing in an innovative force to penetrate these economies for financial inclusion. Almost 40 out of 45 countries are actively using new Fintech.

Mobile Money in Sub-Saharan Africa

Mobile money payment refers to payment services operated under financial regulation and performed on mobile devices. The introduction of mobile money in sub-Saharan Africa has fostered a radical change in delivering financial services to the region. The coverage of financial systems in the region has significantly improved as well and today it leads the world in mobile money accounts per capita (registered and active accounts), volume of mobile money transactions and mobile money outlets. Mobile money account penetration has increased by around 20% from 2011 to 2014. East African region is leading in mobile money innovation, adoption and usage and Kenya is an excellent example of that.

Mobile based money transfer system M-Pesa (M=mobile, Pesa=money in Kiswahili) was launched by Safaricom and Vodacom, the largest mobile network operators in Kenya and Tanzania in 2007. It allows customers to deposit and withdraw money, pay bills and transfer money to others as well. The service has expanded to other countries like Lesotho, Mozambique, Ghana, Romania, and Albania. It has almost 20.7 million users in Kenya itself. Today Kenya sees one of the highest uses of mobile money at 53 transactions per adult per year.

From financial inclusion to economic development

Fintech is setting the path for the development of a digital economy in Africa. Universal access to finance is a necessity and shouldn’t be a luxury anymore. These changes create an unprecedented opportunity to achieve universal access to finance. Models such as mobile banking, big data credit scoring machine-to machine lending etc are helping to achieve this by reducing costs and risk and enabling reach to the un-banked population and poor in low-density areas, hence providing unparalleled opportunities.

Still, there is a long way to go for Africa as its starting conditions are unsatisfactory and unique. Banking penetration is at only 17% on average, while in developed countries it is more than 60%. This leaves much more scope for new entrants to take over the market. Access to internet stands at a meager 23%, while in developed countries it is around 85%, which makes it difficult for businesses in the region. Therefore, it is the responsibility of the Governments to take appropriate measures and provide at least basic amenities to the people. There is a need to bridge the stark inequality prevalent in African regions for better penetration of technology.

For any country, the small and medium-sized enterprises (SMEs) are essential to its economic development. In Africa as well, SMEs will help its economic bounce-back from the COVID-19 pandemic and Fintech will play an important in this. Digital solutions will give SMEs easy access to finance. At present, SMEs in Sub-Saharan Africa are financially constrained. In Nigeria less than 7% of SMEs have ever taken out a formal loan as formal small business loans are hardly ever approved. But with technology advancement SMEs can acquire financing through Fintech platforms. For example- Nigerian lender Lidya offers digital microloans and disburses loans to small businesses amounting to as little as $150 in 24 hours.

While the region has been largely led my microfinance as an alternate source of finance, FinTech in recent years has facilitated the growth of various types of crowdfunding and peer-to-peer lending as well.

Conclusion

In the coming years Africa can expect that-

- Mobile network operators will be the primary African disruptors

- Rapid Dematerialization will take place

- Convergence will accelerate

- Universal electronic financial services will be achieved

However, to achieve these as well as other goals, well-functioning payment system is required that will reduce the costs of exchanging goods and services in the economy. The demand for many other rudimentary financial services, such as credit services, cross-border payments, investment products, and insurance services has to be tapped by emerging Fintech providers.

As the mobile payment providers have already garnered a significant customer base, they also provide new financial services. Some advanced types of FinTech, focused on lending are also growing throughout sub-Saharan Africa. Traditional banks and insurance must build new capabilities spanning strategy, IT and operations and governance. Disruptors can partner up with traditional banks and insurance companies for economic and regulatory reasons.

The growth of the African financial sector is definitely burgeoning and providing great value to customers and financial institutions but the future of its Financial sector will depend on transformation, innovation, navigating the changing business and ensuring better regulatory environment and structuring conducive partnerships.

Excellent article. Excellent analysis and well written.